Arbitrability of IP Disputes in India

Courts around the world have been systematically enlarging the ultimate scope of alternate arbitration dispute mechanisms. This is due to the fact that it has been witnessed throughout the years that arbitrability of ip disputes has progressively become the default commercial dispute mechanism around the globe.

Thus, it is quite imperative that the scope of alternative dispute mechanisms is widened in order to reduce the burden on courts. But talking about the Indian jurisprudence, on the contrary, it has been encountered that time and again courts have emphatically6 and effectively held that the disputes concerning various Intellectual Property Rights as non-arbitrable.

But why is this case with India? This is due to a pertinent and prime reason that courts often strongly are of the opinion that enforcement of IPR involves the public policy aspect. This effectively means that it would be strong going against the interests of the public if such contentious matter of intellectual rights is made arbitrable.

On the other hand, what makes the possibility of enactment of arbitration difficult is the fact that the Indian domestic statutes such as the Arbitration and Conciliation Act of 1996 and various other IP legislations do not effectively provide a concrete expression.

This concrete expression pertaining to the availability of Arbitration in IP Disputes is not strategically laid out by the aforementioned Acts.

To state the specifics to reinforce the fact, it is to be noted that Section 89 of the code of Civil Procedure, 1908 strategically states that the court has the extreme power to refer the IP matters to ADR. Thus, Courts are given the authority or the extreme power to deem fit and consequently allow arbitration, mediation, or conciliation for the alleged settlement of disputes.

Given the aforementioned authority, Courts have been strongly trying to settle the ADR practices. They have also come up with various tests to strategically and easily determine the arbitrability of various types of disputes. Thus, one can conclude that the arbitration process in India is well laid out by the courts that laid out the tests and measures to effectively determine the arbitrability of disputes.

To cite a case, the case of Booz Allen and Hamilton Inc. v. SBI Home Finance Ltd. Serves as a perfect example. In the aforementioned case, the Supreme Court had strongly held that all the disputes which directly pertain to “right in personam” are arbitrable in nature. On the other hand, for clarity, it was stated that all the disrupts that highly relate to “right in rem” are effectively unsuitable for arbitration.

So, the gist of the aforementioned example gives us a much-needed sneak peek into the world of arbitration in India. It intelligently informs us that a major aspect that determines arbitrability is actually the nature of judgment sought by the aggrieved. This determinative attribute states that if the judgment that is sought by the arrived is against

The current status

To judge the current status of arbitration in India, the latest case of the Delhi High Court Judgment is worthy to be scrutinized. The case of Golden Tobie (P) Ltd. v. Golden Tobacco Ltd., is the case where the defendant had effectively filed an application under Section-8 of the aforementioned act namely Arbitration and Conciliation Act, 1996.

To lay down the facts of the case, the parties had entered into a master long-term supply agreement. Now, by the agreement, the defendant had supplied exclusive brands of the defendant to the Plaintiff. Here, to complicate the matter, the plaintiff had subsequently had entered into a trademark license agreement.

The reason by the plaintiff for the same was stated, he had acquired or had been effectively granted an exclusive non-assignable, non-transferable license. The license gave the power to the plaintiff to strategically manufacture the Defendant’s product.

Here, it was stated by the plaintiff, that despite the humungous operational expenditure and capital spent by the plaintiff to amicably and effectively increase the availability of the Defendant’s products, he was issued a termination notice.

Now here it is to be noted that since the commercial production had not yet begun in strength, the agreement was rightly terminated. Subsequently, it was informed by Defendant, upon receiving another termination letter that the timely payment had not been made.

Thus, this meant, according to the defendant, that the plaintiff had no right to potentially and effectively sell his products or manufacture the exclusive brands in the market. Hence, when this suit was filed, it was decided by the apex court that the matter under consideration will be referred to the sole arbitrator.

Thus, given the aforementioned case, it can be strongly argued that the arbitration in Intellectual property rights matters only arises out of the nature of the dispute. This also reinforces the idea that if the procedures are well in place, they can bring an affirmative impact.

Terms related to the article:

arbitrability of ip disputes in india, arbitrability of intellectual property disputes, arbitration of disputes, civil arbitration, the meaning of arbitration, ip arbitration, intellectual property arbitration, arbitrable disputes, arbitrability of ip disputes, arbitrability of disputes in india, arbitrability of competition law disputes in india.

Talking about the recent announcement compared to the earlier archaic regulations, it is to be noted that as per SEBI’s amendments made to Alternative Investment Funds Regulations, 2012, Venture Capital Funds will need to invest at least 75 percent of investable funds.

Talking about the recent announcement compared to the earlier archaic regulations, it is to be noted that as per SEBI’s amendments made to Alternative Investment Funds Regulations, 2012, Venture Capital Funds will need to invest at least 75 percent of investable funds. But it is to be noted that such investment promotion comes as a series of steps. In October amendments were passed by Sebi that had amended the AIF regulations.

But it is to be noted that such investment promotion comes as a series of steps. In October amendments were passed by Sebi that had amended the AIF regulations.

With a high accommodative stance that was adopted by the

With a high accommodative stance that was adopted by the  It is to be noted that given the recent situation of burgeoning prices, the government needs to step in, soothe the apprehensions of the spenders in the economy. Given the massive recession that was witnessed by India last year, the country is still in the process of recovery.

It is to be noted that given the recent situation of burgeoning prices, the government needs to step in, soothe the apprehensions of the spenders in the economy. Given the massive recession that was witnessed by India last year, the country is still in the process of recovery.

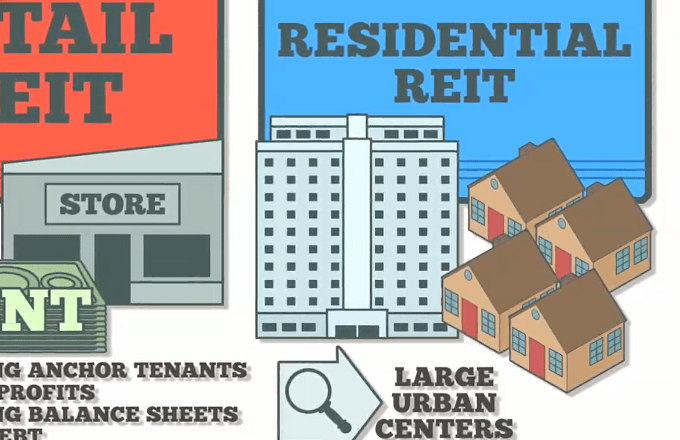

Given the aforementioned importance of infrastructure development in India, EITs and InvITs come into the picture. According to the reports the real estate investment trusts and infrastructure investment trusts have effectively raised capital up to $9.7 billion.

Given the aforementioned importance of infrastructure development in India, EITs and InvITs come into the picture. According to the reports the real estate investment trusts and infrastructure investment trusts have effectively raised capital up to $9.7 billion.

As aforementioned, as the InvITS and REITs will play a significant role in effectively funding the Government’s infrastructure plans, in addition to helping in meeting the asset monetization plans of the government it will also strategically help in meeting the capitalization requirements of banks.

As aforementioned, as the InvITS and REITs will play a significant role in effectively funding the Government’s infrastructure plans, in addition to helping in meeting the asset monetization plans of the government it will also strategically help in meeting the capitalization requirements of banks.

This brings various Payment aggregators like Razor pay, BillDesk and PayU under the ambit of the law as these have set up platforms like MandateHQ, SiHub, and Zion, respectively. These had been operating in the capacity to form or provide a “bridge” for banks to complete the transactions.

This brings various Payment aggregators like Razor pay, BillDesk and PayU under the ambit of the law as these have set up platforms like MandateHQ, SiHub, and Zion, respectively. These had been operating in the capacity to form or provide a “bridge” for banks to complete the transactions. Breaking down the

Breaking down the  it is to be noted that

it is to be noted that

The whole loan app debacle brings to the forefront the need for transparency, better data privacy laws, and a strong vigilance mechanism by the RBI to protect the interest of the public which is currently quite susceptible to harm financially and monetarily.

The whole loan app debacle brings to the forefront the need for transparency, better data privacy laws, and a strong vigilance mechanism by the RBI to protect the interest of the public which is currently quite susceptible to harm financially and monetarily.

given the seriousness of the claim at hand, the CBI has been actively probing the promoters namely Kapil and Dheeraj Wadhawan in the Yes Bank scam. According to the reports, given the pieces of evidence, there is a heavy case of fraud or loss of public money.

given the seriousness of the claim at hand, the CBI has been actively probing the promoters namely Kapil and Dheeraj Wadhawan in the Yes Bank scam. According to the reports, given the pieces of evidence, there is a heavy case of fraud or loss of public money.

Given the objectives of the RBI regulation, it is quite sagacious to mention what might be the impact of such regulations. It is to be noted that the newer regulations have posed some urgency within the financial institutions and the banks.

Given the objectives of the RBI regulation, it is quite sagacious to mention what might be the impact of such regulations. It is to be noted that the newer regulations have posed some urgency within the financial institutions and the banks. Thus, given the nature of the issue and the relevance and importance of such robust censoring and payment system, the recent regulations will greatly safeguard the users’ data. This has all the more important as data privacy concerns are becoming a big concern for users across the globe now. Thus the regulations will emphatically ensure that surveillance and right monitoring will ease out in the investigations.

Thus, given the nature of the issue and the relevance and importance of such robust censoring and payment system, the recent regulations will greatly safeguard the users’ data. This has all the more important as data privacy concerns are becoming a big concern for users across the globe now. Thus the regulations will emphatically ensure that surveillance and right monitoring will ease out in the investigations.

But in the pursuit to eradicate the non-conforming, non-perfect aspect of the asset, will the government forgo the positive potential of the currency? Luckily, the answer might come as good news for the investors, as the government plans to roll out its regulated version, CBDC, in the market.

But in the pursuit to eradicate the non-conforming, non-perfect aspect of the asset, will the government forgo the positive potential of the currency? Luckily, the answer might come as good news for the investors, as the government plans to roll out its regulated version, CBDC, in the market. Thus, one can finally state that the phased introduction of CBDC in India will possibly lead to a more efficient, robust, regulated, and legal tender-based payments option for the public which will be an added advantage. Though, it cannot be denied that there are associated risks with such introduction which, in the light of protecting the welfare of the user, need to be carefully evaluated, but given the potential benefits in the future, one can robustly state that something efficient can be born out of the meticulous efforts of the central bank.

Thus, one can finally state that the phased introduction of CBDC in India will possibly lead to a more efficient, robust, regulated, and legal tender-based payments option for the public which will be an added advantage. Though, it cannot be denied that there are associated risks with such introduction which, in the light of protecting the welfare of the user, need to be carefully evaluated, but given the potential benefits in the future, one can robustly state that something efficient can be born out of the meticulous efforts of the central bank.

The Story of India’s Weak Indian Power Sector

The Story of India’s Weak Indian Power Sector