Understanding Labor Laws & New Labor Codes in India

A labor-intensive country like India has revisited its new labor codes in India and its labor laws. In 2019, the Ministry of Labor and Employment had effectively introduced four Bills to strategically amalgamate 29 central laws.

It is to be noted that these 29 central laws were related to labor laws which were consequently simplified and modernized. Thus, the revision of the laws led to the much-needed revisal and simplification of the labor regulations in a labor-intensive country, like India.

To get a gist of what was strategically regulated in the laws, it is to be noted that wages, social security, and Industrial Relations were thoroughly scrutinized and regulated. On the other hand, attempts were also made to regulate the laws pertaining to health, Occupational Safety, and Working Conditions.

All such aforementioned provisions were codified and enacted effectively as the Code on Wages, 2019; the Occupational Safety, Health and Working Conditions Code, 2020; The Industrial Relations Code, 2020 and the Code on Social Security, 2020

Given the aforementioned acts, what actually were the changes on the ground level that were made by the government? In the labor laws, it was established that the Central Government will be emphatically the ‘appropriate government’. The central government will act as an “appropriate government” for the public sector undertakings.

Here, it is worthy of mentioning that the government will act in such capacity even if the central government’s holding in the entity is less than 50%. Certain industries that have qualified where the central government will act as the appropriate government are the specific industries banking, mines, telecom, and railways.

Talking about the occupational safety and health of the workers, an ‘Inspect ors-cum-Facilitators’ shall be established. This shall be effectively established as the new authority under the Code on Social Security, 2020, the Occupational Safety, Health and Working Conditions Code, 2020, and The Industrial Relations Code, 2020.

ors-cum-Facilitators’ shall be established. This shall be effectively established as the new authority under the Code on Social Security, 2020, the Occupational Safety, Health and Working Conditions Code, 2020, and The Industrial Relations Code, 2020.

The duty of an inspector-cum-facilitator will emphatically be to provide information and reports to industry employees. Thus, the newer labor codes take into consideration the well-being and the interests of the laborers in the economy.

Given that India is a labor-intensive country, with a high contribution of the manufacturing sector in the economy, the address of core issues of the laborers will help in addressing the deep-seated problems and discrepancies that might threaten the efficiency of the labor.

Talking about the social security code, 2020, the code was emphatically introduced to provide social security benefits to the labor class, which are the most deprived social class. This has been strategically done by extending the goals of social security goals to employers and employees.

The code has also worked to emphatically simplify the labor laws by effectively amalgamating various enactments. such as:

The code positively states that the central government will be responsible to frame the social security schemes. This will be done by giving utmost importance to providing benefits under Employees‘ State Insurance Corporation (ESIC) for platform workers, gig workers, and unorganized workers.

In fact, the code also strongly empowers the central government to extend its social security benefit schemes to self-employed persons in the economy. Thus, given that the reins are in the hands of the government, one can maintain that welfare will be positively delivered as the state’s main motive is to deliver justice and protect the welfare of the society.

Thus, given the aforementioned changes and alterations in the new labor codes in India, one can emphatically state that it will lead to redressal of widespread hostilities and discrepancies in the labor system which has been haunting the efficiency and welfare of the labor class.

Given that the government will be gaining reins in the matters of labor laws, one can expect significant improvement in the conditions of the labor class in India, which is thoroughly deprived of justice and rightful means of survival and sustainability.

The act garners all the more important due to the fact that the labor class has suffered inexplicably due to the pandemic that has exacerbated the woes of the labor class. Thus, the new labor code emphatically introduces various special provisions for accommodating better regulations for industries.

This is being done by establishing flexible norms and allowing the industries to be flexible to foster efficiency and commitment to the work. Further, one can state that the ambiguity surrounding certain provisions has been cleared with clear codification and consolidation of the laws.

In fact, it can be positively stated that the codification and consolidation of such laws have positively led to the expansion of the ambit and effective applicability of the laws. Thus this has increasingly helped with ease of compliance and removal of an unnecessary multiplicity of definitions.

Thus, consequently, the reluctance that had seeped into the system due to inefficient and uncodified roles of the overlapping of authorities has been thoroughly removed.

What is more one can positively state about the newer labor code is that the new set of rules will definitely and positively empower the relationship between the employee, the employer, and the government, which will lead to faster resolution of the issue that plague the labor class.

This will also be bn=beneficial for the employees if the labor class is appreciative of the system and thus, ultimately their employer. Thus, in totality, the newer laws will definitely lead to a positive long-term impact on the labor industry and will strengthen further contribute towards the idea of ease of doing business in the economy.

Given that the economy is still in the nascent stage of its recovery and is under threat from the newer variant namely omicron, a little breather for the employees and the employers will contribute highly to the industry’s revival.

Terms related to the article:

new labor codes, labour code, new labour code 2020, new changes in labour laws in India, labour code on wages, labour law codes, the impact of new labour codes in India, the new labour codes, new labor codes in India, labour code in India, new labour codes India.

In fact, according to various analysts and researchers, it has been found that reconstruction of the company is a better way out of the bankruptcy debacle. According to the reports, creditors can effectively gain a potential 52 cents on each dollar owed when a company is strategically restructured.

In fact, according to various analysts and researchers, it has been found that reconstruction of the company is a better way out of the bankruptcy debacle. According to the reports, creditors can effectively gain a potential 52 cents on each dollar owed when a company is strategically restructured. Reconstruction, on the other hand, is quite beneficial for the creditors themselves. This is due to the pertinent fact that the creditors can significantly negotiate equity stakes in the new firm. This negotiation can be carried out in the form of payment for outstanding debt.

Reconstruction, on the other hand, is quite beneficial for the creditors themselves. This is due to the pertinent fact that the creditors can significantly negotiate equity stakes in the new firm. This negotiation can be carried out in the form of payment for outstanding debt.

The Reserve Bank of India, in a recent turn of events, has proposed the rollout of the Prompt Corrective Action (PCA) Framework for the

The Reserve Bank of India, in a recent turn of events, has proposed the rollout of the Prompt Corrective Action (PCA) Framework for the  But will such corrective actions be beneficial in the long run? It is to be noted that through a critical evaluation of the banking system, it has been seen that out of the total number of banks that were effectively placed under the PCA framework, about 11 banks have already come out.

But will such corrective actions be beneficial in the long run? It is to be noted that through a critical evaluation of the banking system, it has been seen that out of the total number of banks that were effectively placed under the PCA framework, about 11 banks have already come out.

The other trend on which the future of CBDC depends is the building network of countries across continents. This shows the brighter side of the story as on 14 July the European Central Bank had confirmed the launch of its digital euro.

The other trend on which the future of CBDC depends is the building network of countries across continents. This shows the brighter side of the story as on 14 July the European Central Bank had confirmed the launch of its digital euro. Another classification is wholesale and retail CBDC. It is to be noted that wholesale CBDCs work by putting existing central bank reserve accounts effectively onto a blockchain. Thus, by the process of tokenizing the central bank money, one can emphatically improve the efficiency of cross-border payments.

Another classification is wholesale and retail CBDC. It is to be noted that wholesale CBDCs work by putting existing central bank reserve accounts effectively onto a blockchain. Thus, by the process of tokenizing the central bank money, one can emphatically improve the efficiency of cross-border payments.

historical development of the

historical development of the

With the increasing popularity of the tech companies and corporations, it has been seen how the tech world is increasingly dealing with the cases such as the ola uber pricing issue and the other google antitrust allegations.

With the increasing popularity of the tech companies and corporations, it has been seen how the tech world is increasingly dealing with the cases such as the ola uber pricing issue and the other google antitrust allegations.

One fact that is worthy of being mentioned is that the

One fact that is worthy of being mentioned is that the  In addition to creating utilities and employment in the retail sector, one will also witness the increase in employment generation in allied sectors. Talking about the gender disparity in India, retail sector up-gradation will also lead to more employment of women as the retail industry is one of India’s largest employers of women.

In addition to creating utilities and employment in the retail sector, one will also witness the increase in employment generation in allied sectors. Talking about the gender disparity in India, retail sector up-gradation will also lead to more employment of women as the retail industry is one of India’s largest employers of women. The government’s response too for such a sector has been accommodating. This has been seen due to the approval that was garnered by the government for its revelation of its accommodating policies in the financial budget 2022. However, various aspects of the same remain untouched.

The government’s response too for such a sector has been accommodating. This has been seen due to the approval that was garnered by the government for its revelation of its accommodating policies in the financial budget 2022. However, various aspects of the same remain untouched.

But it is to be noted that China isn’t exactly like the US in the financial year 2008. These have various reasons, firstly, the reach and impact of the USA were far much more than China, at least in terms of currency.

But it is to be noted that China isn’t exactly like the US in the financial year 2008. These have various reasons, firstly, the reach and impact of the USA were far much more than China, at least in terms of currency. The contagion effect means that turmoil or crisis in one large corporation can easily spread to others. these fears have resurfaced due to the nightmares of the Lehman Brothers crisis that had had the worst contagion effect on the other major financial institutions too. These

The contagion effect means that turmoil or crisis in one large corporation can easily spread to others. these fears have resurfaced due to the nightmares of the Lehman Brothers crisis that had had the worst contagion effect on the other major financial institutions too. These

But has the insolvency takeover led to any significant suppression of descent? Perhaps not. many individuals, especially the

But has the insolvency takeover led to any significant suppression of descent? Perhaps not. many individuals, especially the  It is no news that IBC was effectively passed and implemented for the successful resolution of the insolvency cases in the economy and to effectively present time-bound resolution of the same.

It is no news that IBC was effectively passed and implemented for the successful resolution of the insolvency cases in the economy and to effectively present time-bound resolution of the same.

Thus, it can be argued that the issue of improving the digital lending sector should be viewed with the primary lens of consumer protection.

Thus, it can be argued that the issue of improving the digital lending sector should be viewed with the primary lens of consumer protection. Talking about business lending, there are key building blocks of lending and are extensively used in supply chain financing. Given the nature of the business, it is to be noted that largely finances flow to the supplier accounts which are paid back through an intermediary account.

Talking about business lending, there are key building blocks of lending and are extensively used in supply chain financing. Given the nature of the business, it is to be noted that largely finances flow to the supplier accounts which are paid back through an intermediary account. Given the already existing framework, India today stands tall to offer its citizens and businesses the benefits of universal credit access.

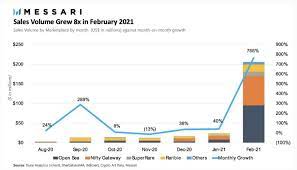

Given the already existing framework, India today stands tall to offer its citizens and businesses the benefits of universal credit access. Given its recent nature, it is quite extraordinary that it has recorded such a humungous growth. This also corroborates the fact that NFT is on the rise and is just in its nascent stage of development, mustering all the growing popularity in the global market.

Given its recent nature, it is quite extraordinary that it has recorded such a humungous growth. This also corroborates the fact that NFT is on the rise and is just in its nascent stage of development, mustering all the growing popularity in the global market. It is to be noted that NFTs that are digital creative works are actually premised on blockchains which work quite similarly to crypto. Blockchain technology which is quite permanent and has unchangeable digital ledgers provides the user the security of recorded transactions that reveal history.

It is to be noted that NFTs that are digital creative works are actually premised on blockchains which work quite similarly to crypto. Blockchain technology which is quite permanent and has unchangeable digital ledgers provides the user the security of recorded transactions that reveal history.